The three-bucket money hack that stops you going backwards

One account can’t do four jobs. Split your cash into Liquidity, Growth and Legacy and watch stress drop fast.

Most people aren’t bad with money. They’re just running their entire financial life out of one messy pool.

That single account is expected to pay bills, handle emergencies, fund holidays, and build wealth. So when life happens (because it always does), you raid “savings”, pause investing, or reach for the credit card. Progress resets. Stress spikes.

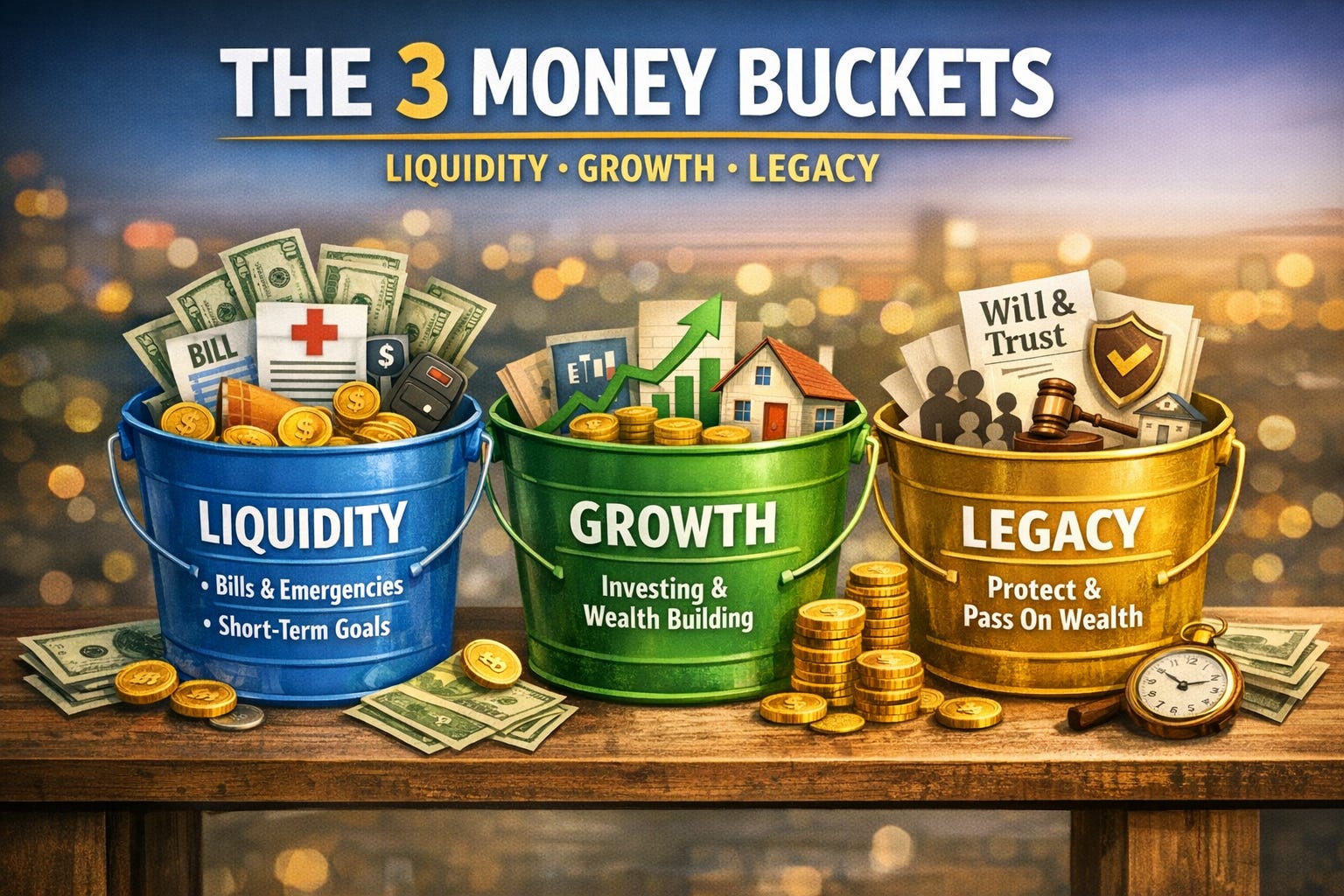

APReview’s fix is simple: three buckets, three jobs.

Liquidity = covers life + protects you from shocks

Growth = turns surplus into wealth over time

Legacy = protects and transfers what you’ve built

When each bucket has a clear purpose, you stop robbing the future to pay for the present.

The rule that changes everything: one bucket, one job

Here’s the trap: if everything sits in one place, every decision becomes a trade-off.

A surprise bill becomes debt

A holiday wipes out “savings”

Investing becomes “later”

And “later” never arrives

A bucket system removes the ambiguity. Each dollar gets a job before it’s spent.

Quick self-check (2 minutes)

If an unexpected $1,500 expense hit this week, would you:

dip into savings,

sell investments,

or use a credit card?

If you’d sell investments or swipe the card, you don’t need motivation — you need boundaries.

Bucket 1: Liquidity (sleep-at-night money)

Job: keep you stable and flexible.

What goes here

Bills account: rent/mortgage, utilities, groceries, fuel, insurance

Emergency fund: separate buffer for genuine “oh no” moments

Short-term goals: holidays, rego, repairs, school costs, renos (next 6–18 months)

What doesn’t

shares/ETFs/crypto (anything that can drop right when you need it)

How much is enough?

A sensible benchmark is 3 months of essential living costs. Many people aim for 3–6 months, especially with dependants or variable income. If that feels huge, start with one month, it changes your decision-making fast.

Where to keep it

High-interest savings (clear separation, easy access)

Offset account (if you have a mortgage and offset support) — reduces interest and stays accessible

Avoid this trap: “My credit card is my emergency fund.”

That’s not a buffer — that’s an expensive loan. If you can’t clear it monthly, interest becomes a permanent leak in your cash flow.

Bucket 2: Growth (make-your-money-work money)

Job: build options for future you.

Two non-negotiables:

It will move up and down

It’s not for next month’s problems

What goes here

ETFs/shares (easy to start, scalable)

Investment property (bigger entry costs, bigger commitments)

Managed funds (watch fees)

Higher-risk assets (fine in small doses — don’t make it the whole plan)

Shares vs property — the real difference

For most Australians it’s not ideology, it’s the start line:

shares: you can begin small

property: deposit + stamp duty + costs + buffers

Neither is “best”. The best option is the one you can hold through cycles without panic-selling.

Offset vs investing

offset = certainty, flexibility, interest savings

investing = higher long-run potential, but volatility + time required

Many households do both: strong buffer + healthy offset + consistent investing.

Bucket 3: Legacy (long-game money)

Job: protect, optimise, and transfer wealth.

Legacy is where you reduce friction:

Protection: insurance, risk management, asset safety

Efficiency: reduce avoidable tax/fee leakage (with advice)

Transfer: estate planning so assets move cleanly to the right people

Superannuation often sits here

For many Australians, super is the default long-game vehicle because of its long horizon and tax settings (rules and thresholds apply).

Property can mature into legacy

Often it starts as growth, then shifts to legacy as debt falls and the focus moves from “growth” to reliable income.

Structures matter — early

Trusts, companies and estate planning can be powerful, but changing structures later can be costly. If you’re building meaningful assets, get licensed tax/legal advice early to avoid expensive do-overs.

The mistakes that keep high earners stuck

Too much cash “just in case” (safety quietly becomes stagnation)

Treating volatile assets like savings (you’ll need it when markets are down)

Investing before a buffer exists (life forces you to sell at the worst time)

Waiting for the perfect moment (momentum beats perfection)

The weekend setup (simple and done)

1) Create/rename accounts by purpose

Bills

Emergency fund

Short-term goals

Investments (growth)

2) Automate the flow (pay yourself first)

On payday:

fund bills + buffer

then growth

then legacy (often super/long-term allocations)

3) Review every 90 days

Income, rates, expenses, goals — adjust transfers, move on.

Punchline: separate buckets, clear purpose, less panic, better decisions.

General information only. Consider licensed advice for your situation, especially for tax and structuring.